.png)

More Australians Now Have The Savings To Consider SMSF Property

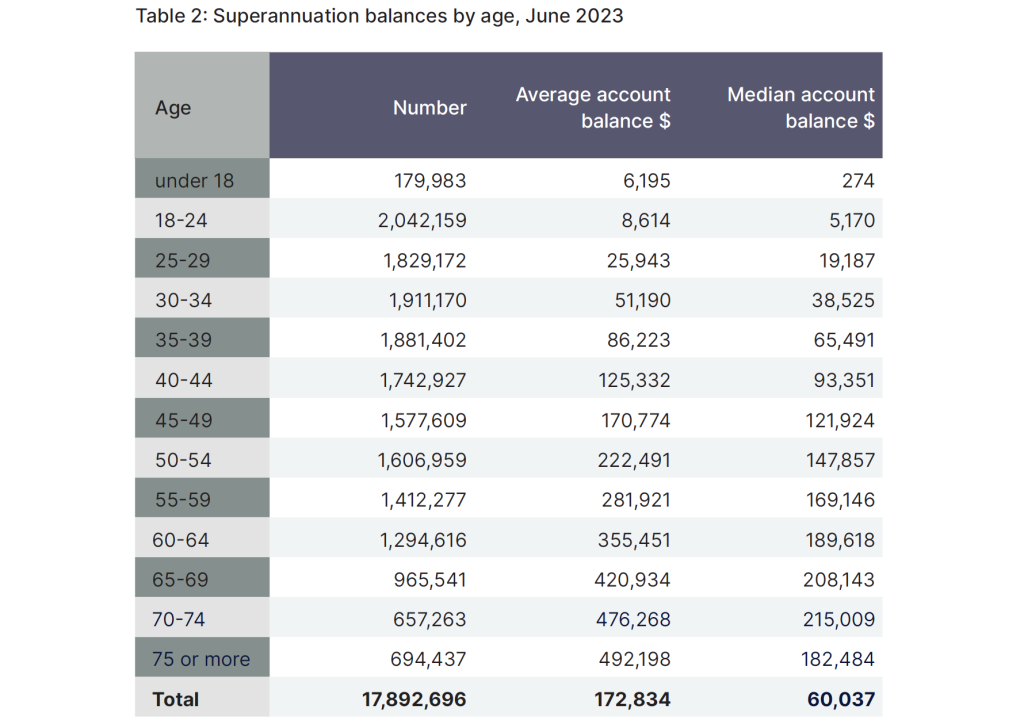

Australians are holding more money in superannuation than ever before. According to the latest research from the Association of Superannuation Funds of Australia, average superannuation account balances reached a record high of $172,834 as of June 2023. For many Australians, this milestone represents more than just progress towards retirement – it creates new opportunities to think strategically about how super is invested.

One option gaining renewed attention is property investment through a self-managed superannuation fund (SMSF). While SMSFs are not suitable for everyone, rising balances mean more Australians now have the savings base required to consider whether SMSF property could play a role in their long-term wealth strategy.

Why higher super balances matter

Building sufficient superannuation savings has long been a barrier to establishing an SMSF, particularly where property is involved. Property transactions typically require meaningful deposits, ongoing expenses and careful liquidity planning. With average balances now at record levels, a larger cohort of Australians may be in a position to assess whether an SMSF structure is viable.

Higher balances can improve flexibility. They may allow trustees to diversify assets, manage cash flow more effectively, and meet the regulatory and lending requirements associated with property investment. Importantly, this does not mean SMSF property is suddenly appropriate for everyone, but it does mean the conversation has shifted from ‘out of reach’ to ‘worth exploring’ for many households.

The appeal of SMSFs for property investors

One of the key attractions of SMSFs is control. Trustees have direct oversight of investment decisions, rather than relying on a pooled fund manager. For Australians who understand property markets and prefer hands-on decision-making, this can be appealing.

SMSFs can also support diversification. Many traditional super funds have heavy exposure to equities and fixed income. Property can add a different asset class to the mix, potentially smoothing returns over time, although diversification works best when assets behave differently across market cycles.

Property held within an SMSF can generate rental income, which contributes to fund cash flow, as well as potential capital growth over the long term. When managed appropriately, this combination can support retirement objectives, particularly as trustees transition from accumulation to pension phase.

Another advantage is the ability to invest in commercial property. SMSFs can purchase premises used by a member’s business, provided the lease is on arm’s-length terms and meets superannuation rules. For business owners, this can allow rent to be paid into super while maintaining separation between personal and business finances.

Borrowing and SMSF lending considerations

SMSFs can borrow to purchase property, but only through a limited-recourse borrowing arrangement. These structures are more complex than standard home loans and come with stricter requirements. Lenders typically require larger deposits, lower loan-to-value ratios and strong cash flow buffers within the fund.

Because the lender’s security is limited to the property itself, SMSF loans are often assessed conservatively. Trustees need to demonstrate the fund can meet repayments, expenses and periods of vacancy without relying on additional borrowing or inappropriate contributions.

This makes professional advice critical. SMSF lending involves superannuation law, property risk and finance structuring, all of which need to align.

Risks and challenges to consider

Despite growing interest, you should be aware that SMSF property investing carries risks. Liquidity is one of the most important. Property is illiquid, which can make it difficult to fund unexpected expenses, pension payments or member exits. Trustees must plan well in advance to ensure sufficient cash is available.

Compliance is another consideration. SMSFs are tightly regulated and breaches can result in penalties, forced asset sales or loss of concessional tax treatment. Trustees are responsible for ensuring all investments meet the sole purpose test and other legislative requirements.

Market risk also applies. Property values can fall and performance varies significantly by location and property type. Geographic concentration can magnify this risk if a large portion of the fund is tied to a single asset in one market.

Finally, SMSFs require time and engagement. Trustees must be comfortable with ongoing administration, reporting and decision-making responsibilities.

Why strategy matters more than ever

Rising super balances may make SMSF property investing more accessible, but accessibility should not be confused with suitability. Property works best in super when it fits within a broader retirement strategy, not as a standalone decision driven by familiarity or past performance.

Trustees should consider how property interacts with other assets, how it supports long-term income needs and whether the fund can remain flexible as circumstances change. What works during accumulation may not work as retirement approaches.

Getting the right advice

For Australians considering SMSF property investing, collaboration is essential. Accountants, financial advisers and mortgage brokers each play a role in assessing feasibility, structuring finance and ensuring compliance.

At Shore Financial, we work with clients and their advisers to help assess SMSF lending options and structure finance appropriately. With super balances at record highs, more Australians may now have the savings to explore SMSF property investing – but doing so carefully and with the right guidance remains crucial.